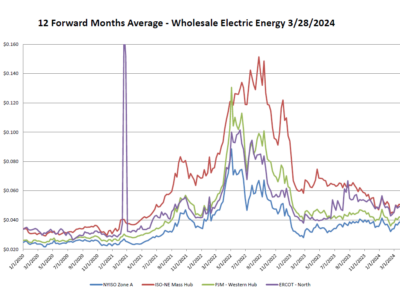

Electricity Markets Northeast forward markets saw a sizable increase over the past week. Markets have continued to remain volatile in response to summer heat and increases in natural gas production. Texas forward markets saw a sizable drop as Hurricane Beryl moved onshore last week. Continue Reading

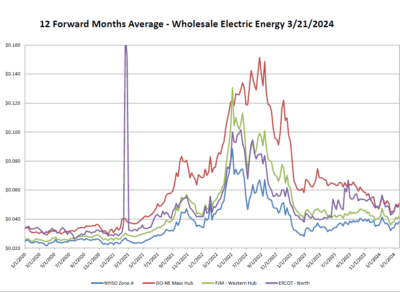

Electricity Markets In spite of market volatility and warm temperatures, NY and PJM forward markets saw sizable drops over the past week, returning to levels that were seen at the beginning of June. Texas also saw sizable drops, now at lowest levels since mid-April. Further forecasted warmth this summer will continue to spur market volatility. Continue Reading

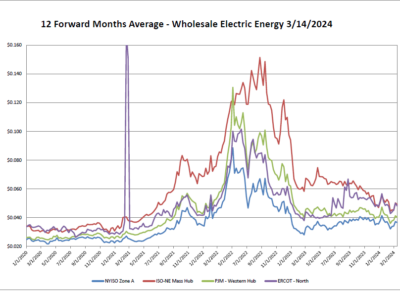

Electricity Markets Forward markets saw a sizable drop over the past week. Expected demand was not met in response to last weeks heatwave. Volatility in the forward markets has been higher than usual over the past month, and is expected to continue as we head into summer. Continue Reading

Power Management Company, a leading provider of innovative energy solutions, is excited to announce the addition of Lyndsay Quiggle to its team as Executive Sales Manager.Continue Reading

Electricity Markets New England and New York forward markets saw a slight increase over the past week. New England increases mainly driven by an increase in Algonquin basis pricing and an increase in liquid natural gas exports. PJM saw a slight decrease, mainly because of increased cloud cover during last week’s heatwave. Continue Reading

Electricity Markets Forward markets saw increased volatility over the past week. Northeast markets saw a sizable increase week over week, and are at their highest rates since the start of 2023. Markets continue to trend upward and will likely continue trending upward as scorching heat returns to the Northeast next week. Continue Reading

Electricity Markets Forward markets saw a slight increase over the past week. Volatility is beginning to make its way back into the forward markets as we head into the cooling season. The markets continue to trend upward Continue Reading

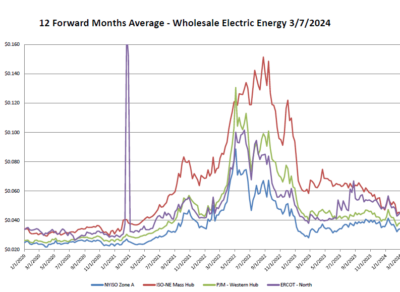

Electricity Markets Forward pricing across all markets saw a sizable drop over the last week. This was largely driven by actual energy demand not meeting market expectation. If expected summer heat materializes, markets could continue to trend upward throughout the summer. Continue Reading

Electricity Markets Forward pricing again increased over the past week, except Texas which saw a slight drop. Gas prices increased over the past week, driving an increase in the electric forward markets. Forward markets have climbed steadily since winter and are expected to keep climbing as this summer is expected to be hot. Continue Reading

Electricity Markets Forward pricing across the Northeast increased over the past week, mainly driven by an increase in near term NYMEX pricing. New England and Texas saw more sizable increases. New England’s was driven by an increase in gas prices, while Texas has seen a sizable spike driven by extreme heat gripping the state. The forecast of a warm summer should keep forward prices increasing in the coming weeks. Continue Reading

Electricity Markets Mild temperatures and low natural gas demand kept NY and PJM flat over the last week. NE rose slightly in lue of expected natural gas production cuts. Texas continues to rise because of continued heat and rapid load growth Continue Reading

Electricity Markets Markets were flat over the last week except Texas, which saw a sizable increase as a heatwave continues to grip the South Continue Reading

Electricity Markets Forward markets stayed mostly flat over the past week. Texas did see an increase as springtime heat returned to the south. Warmer weather in the coming weeks could put upward pressure on forward pricing. Continue Reading

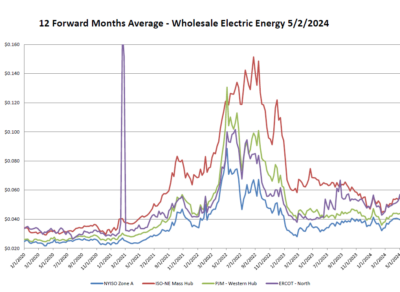

Electricity Markets Forward markets increased slightly over the past week, continuing the longer term trend of slow market gains. Forecasts of a warm summer and electric demand increases in outward years are putting upward pressure on electric pricing in 2025 and beyond. Continue Reading

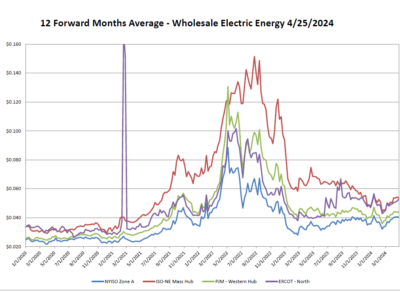

Electricity Markets Forward markets stayed flat over the past week, ending the 4 week run of market gains. Capacity uncertainty and gas production cutbacks loom large into the back half of 2024, but gas storage remains strong Continue Reading

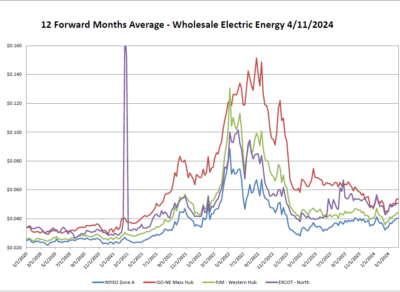

Electricity Markets All forward markets increased week over week, continuing the trend of the past few weeks of market gains. Gains come on the heels of news of a possible warmer summer and production cutbacks Continue Reading

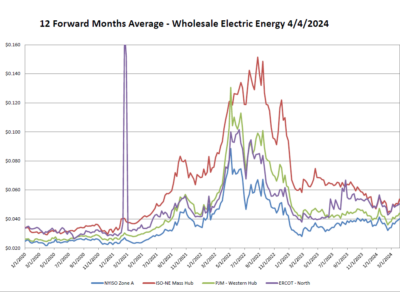

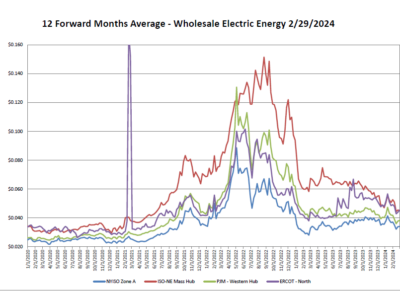

Electricity Markets Forward markets stayed flat over the past week. Market outlook for the coming spring remains good amid strong gas storage surplus Continue Reading

Electricity Markets Forward markets increased over the past week, to highest levels in nearly 2 months. A forecast of a warmer summer could cause markets to tighten up in the coming weeks as we head into spring Continue Reading

Electricity Markets Markets dropped slightly over the last week, the first decrease seen week over week in a few weeks. Despite announcements of further gas production cuts, markets dropped in response to continued mild weather and decreased gas demand. Continue Reading

Electricity Markets Markets moved upwards for the second consecutive week, largely driven by recent announcements of cuts in natural gas production. Continue Reading

Electricity Markets Slight upward movement in forward markets over the past week. ERCOT saw a more sizable increase, and could see larger increases in the coming weeks compared to the Northeast if there is warmer weather. Continue Reading